GENIUS Act Passes Senate, Paving the Way for Landmark US Crypto Legislation

Today (June 17, 2025), the United States Senate voted 68–30 to pass the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act — a landmark piece of legislation that establishes the first comprehensive federal framework for stablecoin regulation. The bill represents a historic step toward broader digital asset oversight, signaling the strongest congressional action to date on crypto policy.

The Senate’s passage of GENIUS now triggers the next phase: conferencing with the House of Representatives. This process will reconcile the GENIUS Act with the House’s Stablecoin Transparency and Accountability for a Better Ledger Economy (STABLE) Act. Although the two bills differ in structure and scope, both reflect a growing bipartisan understanding that stablecoins — blockchain-based tokens typically backed by one or several fiat currencies — require tailored regulation to protect consumers, ensure market resilience, and cement US leadership in digital financial infrastructure.

The GENIUS Act is more than just a stablecoin bill. It marks a clear turning point in US digital asset policy. Rather than relying on piecemeal actions and legal battles, Congress is now laying the foundation for a proactive, legislative approach to oversight. As lawmakers in both chambers work toward a unified framework, GENIUS represents the most consequential step yet in shaping how digital assets will be governed both in today’s market and in the future of financial innovation.

Key takeaways

- The US Senate has passed the GENIUS Act — the first crypto-focused bill to clear either chamber of Congress. This landmark legislation establishes a comprehensive federal framework for regulating fiat-backed stablecoins, combining federal oversight with state flexibility. Key provisions include a dual licensing regime, strict 1:1 reserve backing in high-quality liquid assets, mandatory audits, consumer protections, and anti-money laundering (AML) and sanctions compliance requirements.

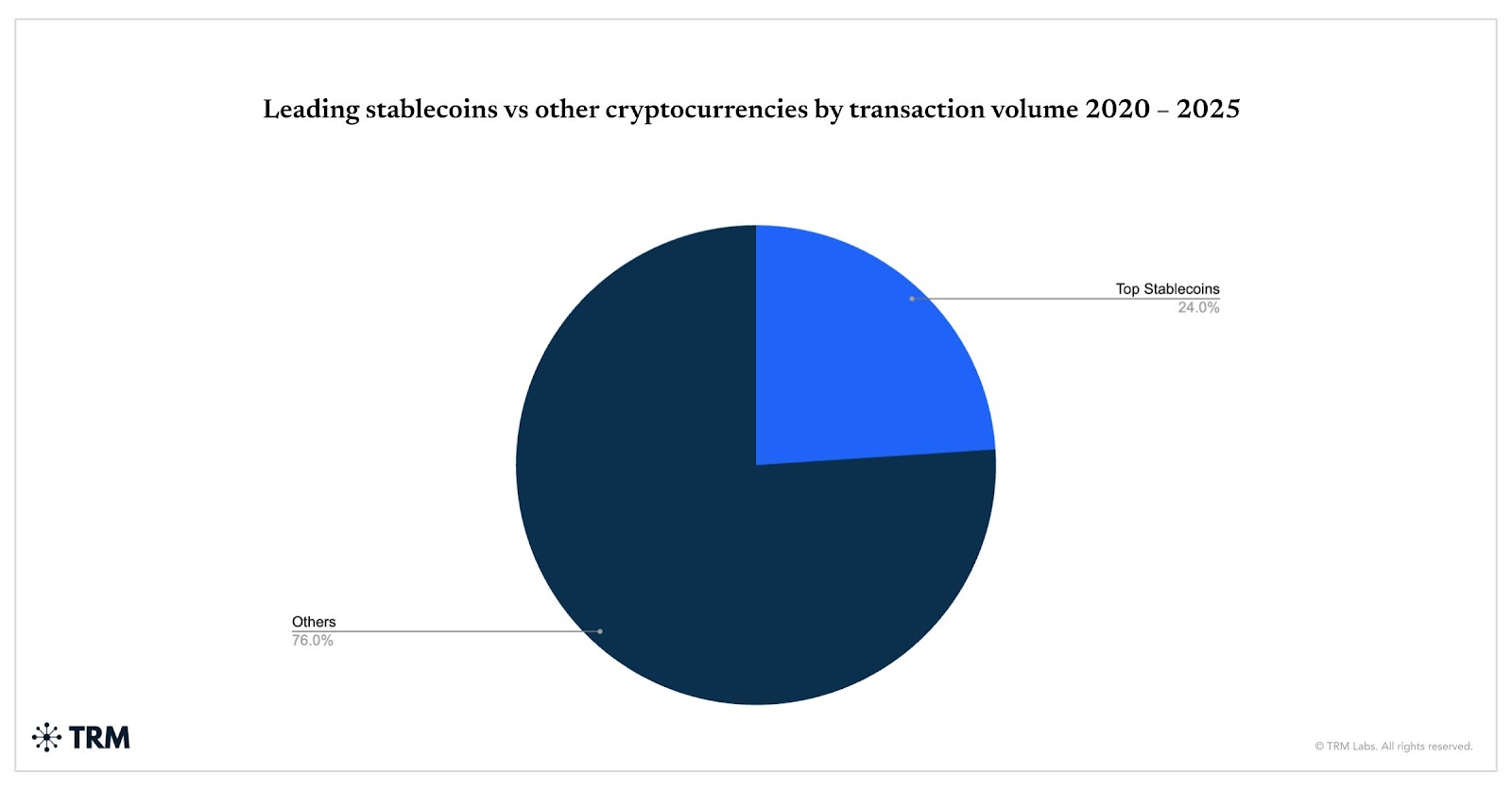

- Stablecoins accounted for 30% of all crypto transaction volume in the first quarter of 2025. More than 90% of fiat-backed stablecoins in circulation are pegged to the US dollar.

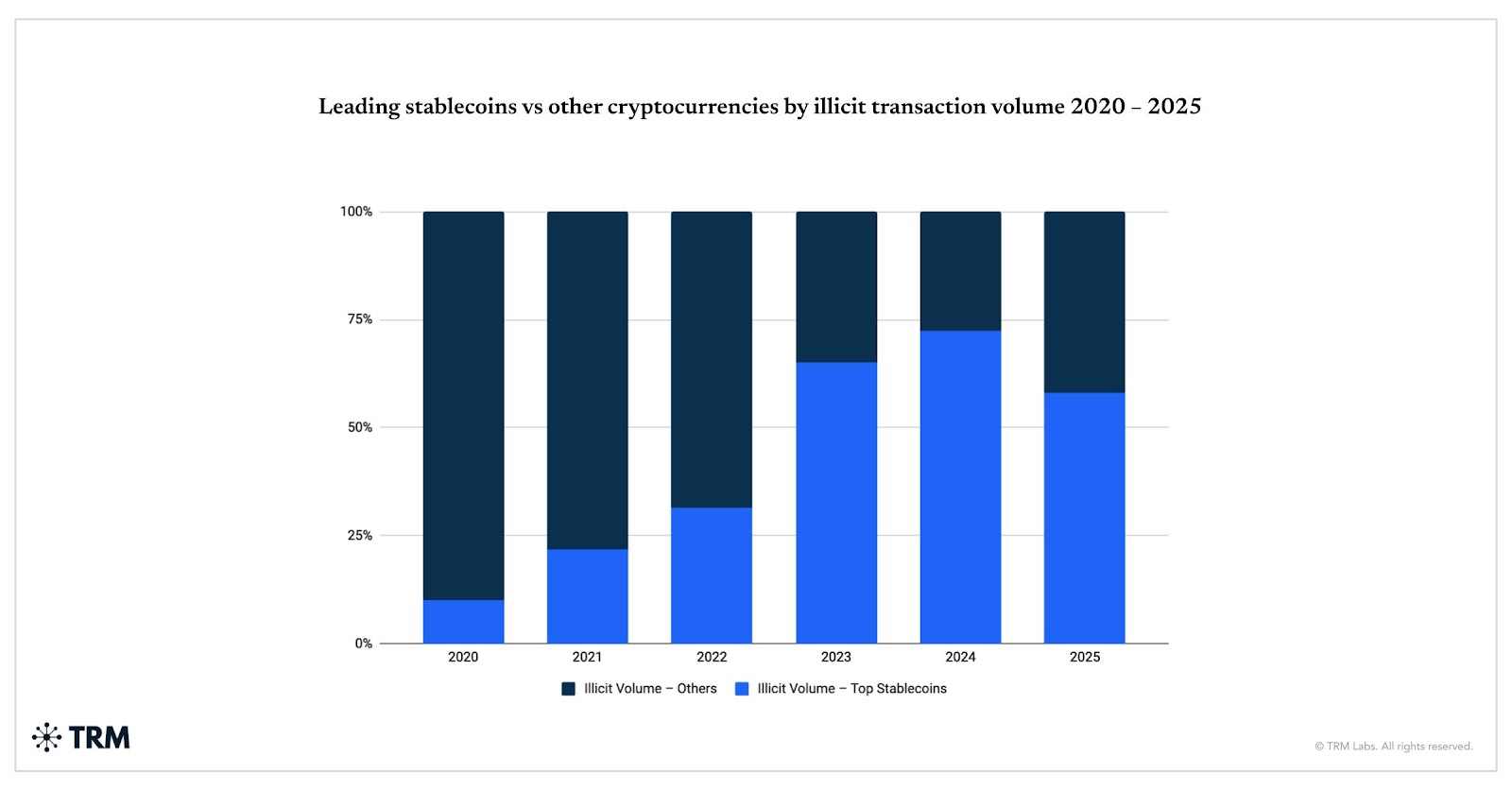

- Although TRM estimates that 99% of stablecoin activity is licit, their speed, scale, and liquidity have made them appealing for illicit uses, including ransomware payments, fraud, and terrorist financing.

- Public-private partnerships like the T3 Financial Crime Unit have proven critical to disrupting illicit finance. In 2025 alone, T3 efforts supported the seizure of over USD 200 million linked to criminal activity.

- With the GENIUS Act now passed in the Senate, lawmakers must reconcile it with the House’s STABLE Act. Key issues for conference include the structure of federal oversight, coordination with state regulators, and the regulatory treatment of algorithmic stablecoins.

The stablecoin landscape in 2025

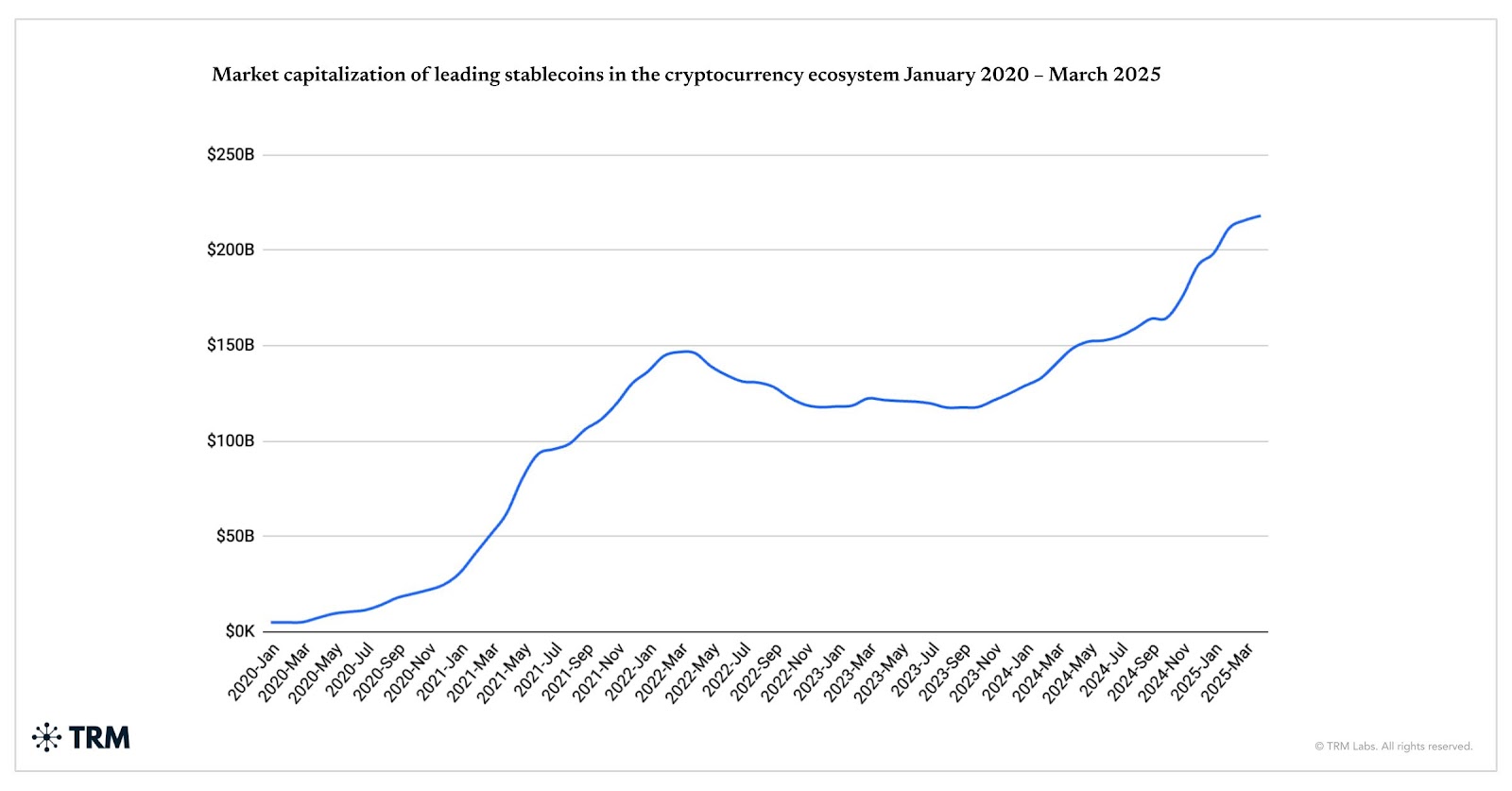

The GENIUS Act’s passage comes amidst accelerating stablecoin use and adoption. TRM data shows that stablecoins have become a core feature of digital asset markets — not just for trading, but for payments, remittances, and savings as well. In 2024 and 2025, leading stablecoins consistently made up at least 4% of total cryptocurrency market capitalization. Their adoption is accelerating across Latin America, sub-Saharan Africa, and parts of Southeast Asia, where individuals and businesses are turning to stablecoins for more reliable access to US dollars, faster cross-border transactions, and alternatives to traditional financial systems.

Today, TRM estimates that over 90% of fiat-backed stablecoins in circulation are pegged to the US dollar. That includes major players like USDC, whose issuer Circle became the first stablecoin company to be publicly listed on the New York Stock Exchange on June 5, 2025 — a major milestone for the space. Other top dollar-pegged stablecoins include USDT and FDUSD, underscoring the growing role of USD-backed digital currencies in global financial activity.

Licit vs. illicit use

Stablecoins are primarily used for legitimate purposes, providing a stable, dollar-linked bridge between more volatile assets like Bitcoin and traditional payment systems. TRM’s analysis of 2024 transaction data found that more than 99% of stablecoin volume was licit, supporting a wide range of use cases including payments, participation in decentralized finance (DeFi), digital commerce, and cross-border remittances.

Still, like any value transfer mechanism, stablecoins have also been misused in illicit activity. Their speed, liquidity, and perceived stability have made them attractive for ransomware payments, terrorist financing, romance and investment scams, sanctions evasion, over-the-counter (OTC) fraud, and large-scale laundering. TRM analysis found that, in Q1 2025, stablecoins accounted for 60% of illicit transaction volume across the crypto ecosystem.

According to TRM’s 2025 Crypto Crime Report, stablecoins remain the preferred asset for terrorist financing and other forms of illicit activity—despite growing interest in privacy coins like Monero. Their appeal lies in the same qualities that attract lawful users: price stability and ease of use for payments. But unlike cash or privacy-enhanced assets, stablecoins operate on public blockchains, making their movement traceable with the right tools. This transparency, when paired with advanced blockchain analytics, often makes stablecoins more visible than traditional financial instruments. Beyond traceability, many stablecoin issuers also have the authority to freeze, burn, or reissue tokens, giving them a unique ability to neutralize illicit proceeds or return stolen funds to victims or government authorities.

Why this matters

Stablecoins now play a foundational role in the digital asset ecosystem. According to TRM data, they accounted for 30% of all crypto transaction volume in Q1 2025. Their appeal lies in combining the speed and accessibility of blockchain with the stability of fiat currencies, making them ideal for cross-border payments, savings, and dollar access in high-inflation regions.

Yet, despite their growing utility, the US has operated without a clear federal framework for how stablecoins should be issued, backed, and regulated. The GENIUS Act marks a significant shift — aiming to align consumer protection and financial oversight with the realities of innovation and market demand.

A brief history of the bill

The GENIUS Act was originally introduced in 2023 in response to growing bipartisan concerns over systemic risk, market integrity, and the unchecked expansion of stablecoin issuers operating without clear oversight. Developed with input from federal regulators and industry stakeholders, the bill initially moved slowly, but gained significant momentum after the 2024 US presidential election, advancing rapidly through procedural steps to Senate passage.

Its House counterpart, the STABLE Act, reflects many of the same priorities: clear licensing requirements, mandatory audits, and strict 1:1 reserve backing. With both chambers now advancing parallel proposals, the two bills move into reconciliation — a critical step toward establishing the first comprehensive federal framework for stablecoins.

What’s in the GENIUS Act?

The GENIUS Act proposes a dual-licensing regime for fiat-backed stablecoin issuers, establishing clear federal standards while preserving state-level supervisory authority. This framework aims to bring uniformity to a fragmented regulatory landscape, offering optionality and accountability for issuers.

Key provisions include:

- Federal licensing option

The GENIUS Act establishes a federal licensing pathway for stablecoin issuers. Nonbank issuers with more than USD 10 billion in outstanding stablecoins would fall under the supervision of the Office of the Comptroller of the Currency (OCC), while subsidiaries of insured depository institutions would be overseen by their respective federal banking regulators.

- State license recognition

State-chartered issuers can operate under state oversight, provided their regulatory frameworks are "substantially similar" to federal standards. Issuers exceeding USD 10 billion in circulation must either transition to federal oversight or cease new issuance.

- Mandatory reserve backing

Issuers are required to maintain a 1:1 reserve ratio, backing stablecoins with high-quality liquid assets (HQLAs) such as US dollars, short-term Treasury securities, or central bank reserves. Rehypothecation or reuse of these reserves is generally prohibited.

- Audit and attestation requirements

Stablecoin issuers must provide monthly public disclosures of reserve compositions. Issuers with more than USD 50 billion in outstanding stablecoins are required to submit annual audited financial statements, enhancing transparency and consumer confidence.

- Restrictions on algorithmic stablecoins

The GENIUS Act does not outright prohibit algorithmic or unbacked stablecoins. Instead, it mandates a comprehensive study by the Treasury Department on "endogenously collateralized stablecoins," which are backed by other digital assets created by the same issuer.

- Treasury authority to mitigate risk

The Act grants the Secretary of the Treasury authority to designate foreign stablecoin issuers as noncompliant if they fail to adhere to US regulations. This designation would prohibit centralized digital asset service providers from facilitating the secondary trading of these foreign stablecoins within the US.

- AML and sanctions compliance mandate

All stablecoin issuers are classified as financial institutions under the Bank Secrecy Act (BSA). They are required to implement AML programs, conduct suspicious activity reporting, and comply with Office of Foreign Assets Control (OFAC) regulations.

- Consumer protection measures

The GENIUS Act establishes legal redemption rights, ensuring that stablecoin holders can redeem their tokens at par value. It also mandates operational transparency and prioritizes stablecoin holders' claims over other creditors in the event of issuer insolvency.

- Limitations on stablecoin issuance by non-financial public companies

An amendment, Section 102(b)(2)(B), restricts public companies that are not primarily engaged in financial services from issuing payment stablecoins unless they obtain unanimous approval from the Stablecoin Certification Review Committee. The provision is designed to prevent non-financial firms — such as large technology companies — from issuing stablecoins without undergoing a rigorous vetting process. By requiring high-level scrutiny, this section aims to safeguard financial stability and ensure that only entities with appropriate expertise, oversight, and risk controls participate in the issuance of widely used digital assets.

The bill also includes additional amendments that strengthen the role of state regulators in overseeing stablecoin compliance programs and introduce a phased implementation timeline to support issuer onboarding. Notably, language in Section 303 clarifies that the Treasury’s enforcement authority would be executed “in consultation with appropriate national security agencies,” signaling a strong focus on illicit finance prevention.

If enacted, the final stablecoin bill — passed out of the Senate, the House and signed by the President — would arguably establish, along with stablecoin rules in the United Kingdom (UK), the European Union (EU), the United Arab Emirates, Singapore, and elsewhere, some consistent standards for digital dollar issuance in the world.

{{UK Cryptoasset Regulation – The Government Publishes Plans}}

Crypto regulation in the US and beyond

As the US works to establish federal oversight of stablecoins, other jurisdictions have already implemented national and supranational frameworks designed to regulate the issuance, redemption, and risk management of fiat-backed digital assets. Although approaches vary in structure and scope, most align on core principles: reserve backing, operational transparency, and anti-financial crime safeguards.

- 🇪🇺European Union: MiCA

The Markets in Crypto-Assets (MiCA) framework, which took effect in 2024, is the EU’s first comprehensive regulatory regime for digital assets. MiCA requires stablecoin issuers, referred to as “e-money token” providers, to register with national authorities, maintain full reserve backing, and comply with disclosure obligations. Oversight is centralized through the European Banking Authority, offering a consistent set of standards across all 27 member states. The bloc-wide structure reduces regulatory fragmentation and enables single-passport access to the entire EU market.

- 🇦🇪United Arab Emirates: VARA

Dubai’s Virtual Assets Regulatory Authority (VARA) governs crypto activity through an activity-based framework that differentiates between issuance, custody, trading, and brokerage services. Licensing is tailored to the function and risk profile of each entity, with tiered compliance requirements. VARA also emphasizes ring-fencing of funds and operational segregation — measures designed to mitigate systemic risks while maintaining jurisdictional appeal for global crypto firms.

- 🇸🇬Singapore: Payment Services Act

Singapore’s Monetary Authority (MAS) regulates stablecoin issuers under the Payment Services Act, which includes licensing, minimum capital requirements, and strict AML/Countering the Finance of Terrorism (CFT) obligations. Issuers must demonstrate reserve sufficiency and redemption capability, and are subject to periodic reporting. In 2023, MAS finalized guidance on stablecoin standards, highlighting transparency, cybersecurity safeguards, and consumer protection.

- 🇬🇧United Kingdom: E-money and stablecoin guidance

The UK has proposed extending e-money regulations to include fiat-backed stablecoins. These rules would require stablecoin issuers to hold reserves in liquid, low-risk assets, meet redemption requirements, and implement robust governance structures. The Financial Conduct Authority (FCA) is expected to provide further clarity in 2025, with an emphasis on aligning financial innovation and traditional risk management norms.

And, it has not just been about US federal and global frameworks. Over the last few years, US states have led key regulatory developments around stablecoins, often ahead of federal action. As noted in TRM’s New York State of Mind blog post, in 2022, the New York Department of Financial Services (NYDFS) became the first state agency to issue formal guidance for stablecoin issuers, requiring full 1:1 reserve backing in US dollars or high-quality liquid assets, monthly independent attestations, and clear redemption rights at par value.

Wyoming has taken a different approach, establishing a Stable Token Commission to oversee the issuance of a state-backed stablecoin known as the Wyoming Stable Token (WST), fully backed by US dollars held in state-controlled accounts. Other states, including Texas and Nebraska, have explored regulatory frameworks through legislative or administrative guidance, contributing to a diverse but increasingly aligned state-level patchwork. For more, listen to TRM Talks with Wyoming Stable Commission Director Anthony Apollo here.

GENIUS anti-money laundering provisions and combatting illicit activity in stablecoins

The GENIUS Act contains multiple provisions aimed squarely at combatting money laundering, terrorist financing, and other illicit uses of stablecoins, reflecting Congress’s growing focus on integrating anti-financial crime safeguards into digital asset legislation. These requirements are outlined primarily in Title IV of the bill and emphasize not just compliance, but proactive prevention.

Section 102(a) of the bill states that "the Secretary of the Treasury shall have the authority to prescribe regulations establishing requirements" for the registration and oversight of payment stablecoin issuers. This gives the Treasury broad rulemaking authority to implement the Act’s provisions and build out its supervisory infrastructure.

Although the GENIUS Act reaffirms that issuers are subject to the BSA, the bill specifically empowers Treasury to ensure that issuers have robust AML programs, transaction monitoring capabilities, reporting obligations for suspicious activity, compliance with economic sanctions administered by OFAC and other BSA requirements.

The bill introduces the concept of a “lawful order” (see Section 3(16)), defined as a court- or agency-issued order under federal law that requires a stablecoin issuer to “seize, freeze, burn, or prevent the transfer of payment stablecoins.” Treasury is one of the federal agencies that could issue or enforce such orders under its statutory authority. This effectively gives Treasury and its sub-agencies legal power to block, disable, or neutralize specific stablecoin assets in national security or criminal cases. The bill is missing the specific requirement to “reissue” frozen or burned assets. Such a provision would strengthen a final bill and ensure that funds are returned to victims.

Treasury is also authorized under Section 109 to provide guidance to issuers regarding the submission of periodic reports that demonstrate compliance with operational, financial, and security standards. These reports may include AML metrics, customer due diligence (CDD) processes, and suspicious transaction patterns.

Partnering to combat illicit activity in stablecoins

When it comes to combating financial crime involving stablecoins, arguably even more important than regulatory and legal frameworks are public-private partnerships. The T3 Financial Crime Unit (T3 FCU), a joint initiative from TRON, Tether, and TRM Labs, plays a critical role in the global fight against stablecoin-enabled financial crime. T3 brings together blockchain intelligence, network-level transparency, and asset control capabilities to rapidly detect, trace, and disrupt illicit financial flows across the stablecoin ecosystem.

By combining TRM’s investigative tools with Tether’s asset-freezing authority and TRON’s protocol-level insights, T3 enables real-time collaboration with law enforcement agencies worldwide. This partnership has already supported the seizure of over USD 200 million in illicit proceeds, including funds tied to scams, fraud, and terrorist financing.

As stablecoins become a core layer of global finance, efforts like T3 are essential to ensuring their security, integrity, and lawful use. In 2025 alone, TRM tools have supported dozens of investigations and enforcement actions involving stablecoin misuse, including:

- Tracing cross-chain laundering activity involving USDT and USDC across TRON, Ethereum, and Avalanche

- Flagging ransomware-linked addresses attempting to obfuscate proceeds via stablecoins

- Assisting law enforcement in freezing stablecoin assets before they could be off-ramped

- Working with law enforcement to reissue frozen stablecoin assets to return funds to victims of crime.

With behavioral intelligence and real-time alerts, TRM helps regulators, virtual asset service providers (VASPs), and financial institutions to detect suspicious patterns early, and respond decisively.

What comes next?

With Senate passage complete, the GENIUS Act now enters conferencing — the formal process by which the House and Senate hash out differences. Although both bills — STABLE and GENIUS — share foundational goals such as mandating reserve backing, defining regulatory oversight, and enhancing consumer protections, their technical architectures diverge in critical ways. The conferencing process will require lawmakers to bridge those differences, aligning on questions such as how stablecoin issuers are supervised, which federal agency will lead enforcement, and how federal and state regulators will coordinate their roles.

This phase is both procedural and strategic. A conference committee composed of members from both chambers will be tasked with drafting a unified bill. That version must then return to the House and Senate for final passage; each chamber must approve the same text before the bill can be sent to the President for signature. Given the scope of the policy questions at stake, this process could stretch through the summer legislative calendar.

If a final version of the GENIUS Act is enacted, a new chapter begins: implementation. Federal regulators will be responsible for issuing rulemakings, establishing licensing frameworks for stablecoin issuers, and defining the operational standards required for compliance.

Entities across the financial ecosystem — from fintech startups to established crypto platforms — will need to evaluate their models under the new law. Key implementation questions include how hybrid and algorithmic stablecoins will be treated, which agencies will conduct examinations, and what transition timelines will apply.

In short, conferencing is not just a legislative formality — it is the crucible where the first comprehensive US digital asset law will be forged.

Conclusion: US crypto regulation is coming

Although the GENIUS Act has not yet become law, today’s Senate vote marks the strongest bipartisan momentum to date for federal crypto legislation. For the first time, stablecoins — and the institutions that issue, trade, and custody them — are on a defined path to regulatory clarity. TRM’s analysis finds that stablecoins are increasingly used for payments, savings, and access to dollar-denominated assets in emerging markets. However, they’ve also become embedded in fraud, laundering, and sanctions evasion, reinforcing the need for enforceable guardrails.

The GENIUS Act reflects this dual reality: stablecoins are both a foundational technology and a growing compliance imperative. The message to the market is clear — regulation is coming soon, and it’s taking shape now. As the Act moves into reconciliation with the House’s STABLE Act, lawmakers will define how the final framework balances innovation and oversight — determining the roles of federal and state regulators, how reserve assets are supervised, and how enforcement is carried out.

Once reconciled and passed by both chambers, the law’s implementation phase will begin, ushering in new rulemakings and licensing standards. For VASPs, fintechs, and financial institutions, this is the moment to align with that future. Those who invest in auditability, transparency, and risk infrastructure today will be best positioned to lead in a safer, regulated digital asset economy.

GENIUS Act and stablecoin regulation FAQs

What is the GENIUS Act and why is it significant?

The GENIUS Act is a landmark piece of legislation that establishes the first comprehensive federal framework for stablecoin regulation. The bill represents a historic step toward broader digital asset oversight, signaling the strongest congressional action to date on crypto policy.

How does the GENIUS Act propose to regulate stablecoins?

The Act introduces a dual licensing framework, combining federal oversight with state-level flexibility. Key provisions include mandatory 1:1 reserve backing in high-quality liquid assets, independent audits, restrictions on algorithmic stablecoins, and robust AML and sanctions compliance requirements under the BSA.

Are stablecoins primarily used for illicit activity?

No. TRM’s analysis shows that more than 99% of stablecoin volume is licit, supporting use cases such as payments, decentralized finance, and remittances. Although stablecoins have been misused for illicit purposes due to their speed and liquidity, their traceability on public blockchains enables law enforcement and compliance teams to detect and disrupt criminal activity.

What role does public-private partnership play in combating stablecoin-related crime?

Initiatives like the T3 Financial Crime Unit — formed by TRON, Tether, and TRM Labs — demonstrate the importance of collaboration. By combining investigative tools, asset control capabilities, and protocol-level insights, T3 has supported seizures of over USD 200 million linked to criminal activity in 2025 alone.

What happens next for the GENIUS Act?

Following Senate passage, the bill enters the conferencing stage, where lawmakers reconcile it with the House’s STABLE Act. Once a unified version is finalized and approved by both chambers, federal regulators will begin implementing licensing standards, compliance frameworks, and enforcement protocols.